Auditing the Fed: How Has Average Inflation Targeting Held Up?

Auditing the Fed: How Has Average Inflation Targeting Held Up?

Not great.

Now that the one-year anniversary of average inflation targeting (AIT) has come and gone, I thought it might be fun to discuss how the new framework has performed. As I mentioned last week, there’s no real way to evaluate the Fed’s performance because they have not offered any insights regarding how they are measuring average inflation. But fear not, that just means we will have to channel our inner Sala-i-Martin and check every possibility.1

Okay… maybe not every possibility, but it is possible to check quite a few with only a visit to FRED and a few steps in Excel.

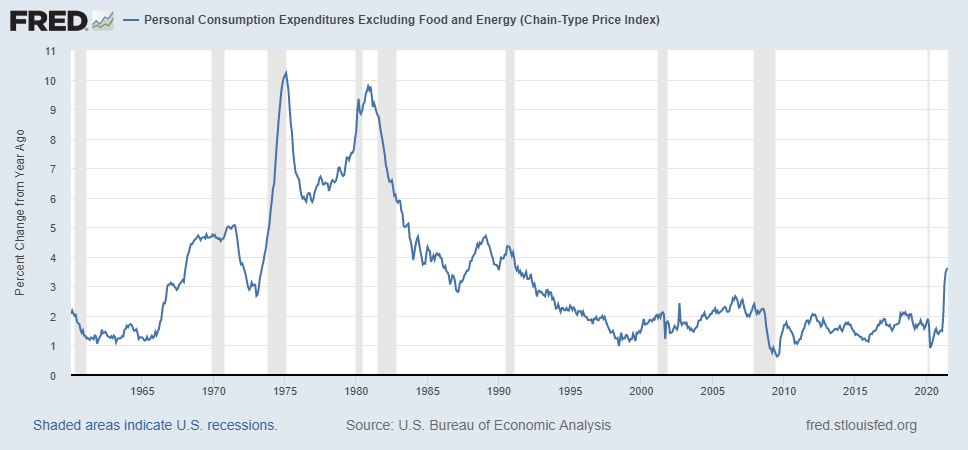

The trick is deciding how the average takes shape. However, there are a few reasonable assumptions that will help hone in on what might otherwise be an insurmountable task. First, it’s highly unlikely the Fed is considering inflation rates that occurred before the ’90s. The extreme nature of the ’70s would only skew the averaging and make their task more difficult.

Second, in what (little) has been said about average inflation targeting, Fed officials have most commonly cited the persistent under-shooting of inflation as motivation for adopting the new framework. Thus it’s most likely that they are not looking beyond the great financial crisis (GFC).

Third, there are two key dates that stand out during this period. In 2012, the Fed officially launched its prior strict inflation targeting framework. And then in December 2015, then-Fed Chair Janet Yellen oversaw the first post-GFC interest rate hike).

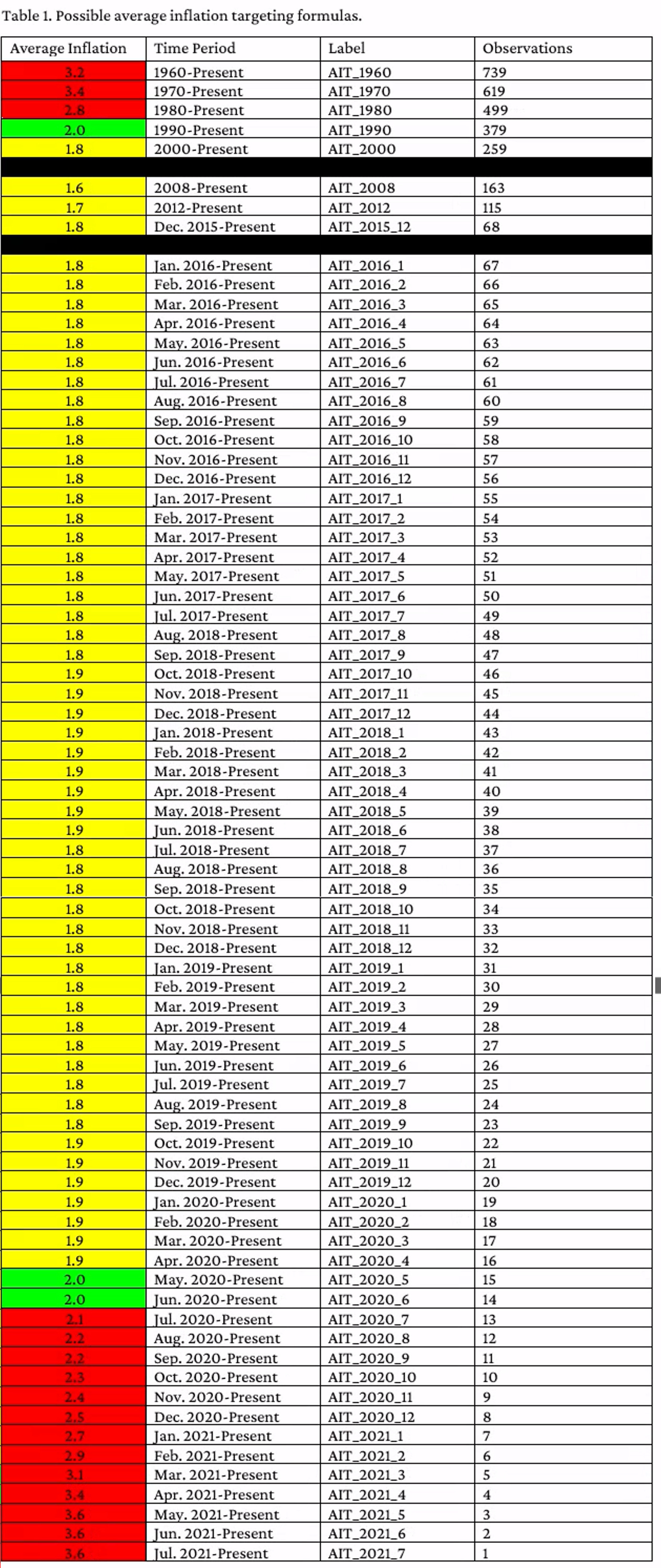

So with that said, I’ll review average inflation from 1960, 1970, 1980, 1990, and 2000 to the present for the sake of robustness. Then, I’ll turn to the periods since 2008, 2012, and December 2015. And finally, beginning with January 2016, I’ll consider monthly intervals (yes, all 67 possibilities) leading to today.

And now for the big reveal!

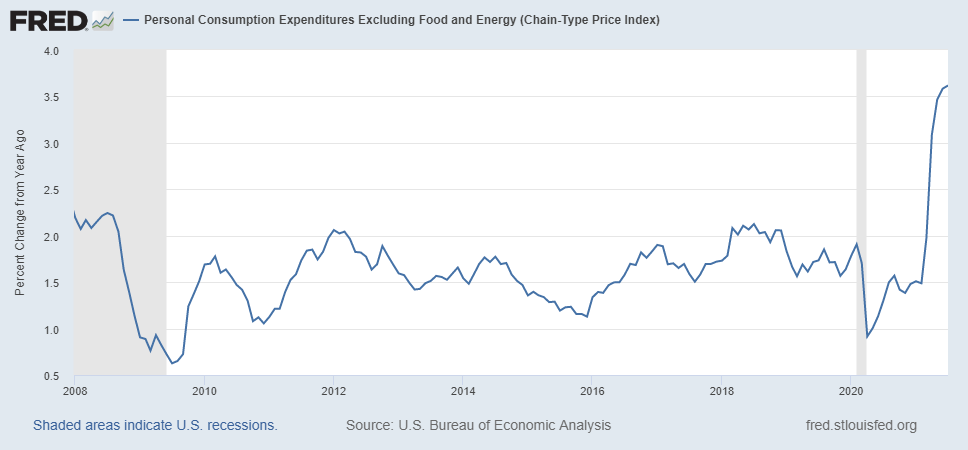

How is the Fed doing at average inflation targetting? Well, not great (see the chart below). The Fed has rarely achieved its two percent average inflation target. It almost had it beginning in May and June of 2020, but it seems to have been a fleeting moment. Even staying within ten basis points has been difficult.

Granted… the Fed could always prove me wrong by providing greater detail about how the averaging is measured.

For anyone interested in the numbers, here are the different averages.

For the unfamiliar, see Xavier Sala-I-Martin’s I Just Ran Two Million Regressions.