The Fed’s Average Inflation Targeting at One Year

The Fed’s Average Inflation Targeting at One Year

If Chair Powell really wants to have the Fed be as transparent as possible, a first step would be to provide the public with a better understanding of the Fed’s plan for averaging inflation.

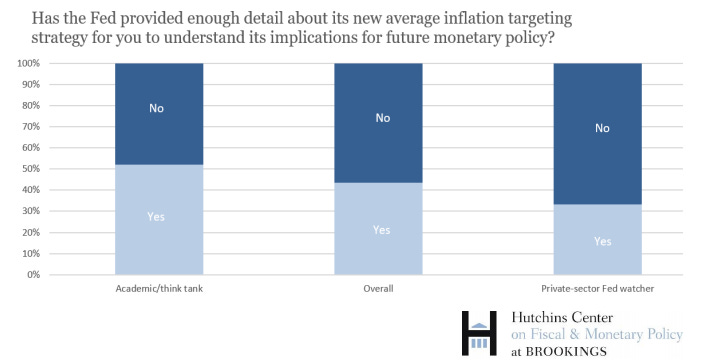

Even though today marks the one-year anniversary of the Federal Reserve’s adoption of their average inflation targeting framework, it might be best if the champagne is put on hold for it is still far from clear if the new program has been a success. In fact, 50 percent of Fed watchers believe the Fed has not provided enough detail about its new strategy (See figure 1).

Figure 1. Uncertainty Amongst Fed Watchers

One year ago, Fed Chair Jerome Powell announced that the Fed would “seek to achieve inflation that averages 2 percent over time,” and thus, “following periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.” In other words, sometimes inflation will be high and sometimes it will be low, but the Fed will try to average it out to 2 percent in the end.

Those frustrated with Fedspeak, or the opaque and confusing language often employed by Fed officials, likely rejoiced when news spread that an averaging formula would be guiding decisions. Considering one need only add up the inflation rates observed over some number of periods and then divide that number by the number of periods observed, it’s a rule that just about anyone can evaluate. And yet, no one really knows how the new framework has been performing over the past year. How can that be the case?

The Fed made headlines when it announced the launch of the new framework after its strategic review, but it didn’t offer much more than the press release. Chair Powell’s speech was exceedingly vague about the plan: neither the time period nor the number of observations being used was shared with the public. In fact, both Chair Powell and Cleveland Fed President Loretta Mester emphasized that the policy is not tied to any specific formula. And that certainly seems to be the case considering Fed Presidents Robert Kaplan, James Bullard, and Patrick Harker all had different criteria in mind when they were asked about how the averaging would be used in practice.

So, while the Fed has finally given itself a rule that the general public can understand, it has simultaneously prevented any reasonable degree of enforcement that would make the rule credible.

This news is especially disheartening considering an average inflation target should force the Fed to make up for past mistakes. As David Beckworth noted in response to the announcement, this move was the first time that a major central bank had implemented a make-up policy. Yet, without any of the specifics in hand, there is no way to know if the Fed will actually make do on the framework’s potential.

Chair Powell explicitly said in his speech that part of the decision was to help anchor inflation expectations. But without any specifics to guide the public’s understanding, this is an anchor that has yet to reach the seafloor. Maybe it will still slow down movements (or, reduce the volatility in expectations), but recent research has shown that clearer communication would improve the performance of the new framework. More so, it would improve the Fed’s credibility.

A defined average would force the Fed to react to past mistakes, but a “flexible” average could be redefined time and time again, so the goalposts are always just out of reach. Disappointed by the news, Norbert Michel wrote last year that, “After basically a decade of being unable to hit its inflation target, the Fed has essentially broadened its definition in a way that ensures it can’t miss.”

Unfortunately though, it seems unlikely that the Fed will shine any additional light on its operations. In fact, history may even be repeating itself. It was 25 years ago when, as David Wessel notes, “Fed officials reached a rough consensus behind closed doors that 2 percent was a good definition of price stability.” Today, the Fed has again kept its decisions behind closed doors. Like how the 2 percent target was eventually made public in 2012, will we need to wait 16 years before a clearer explanation of the averaging formula is made public?

If Chair Powell really wants to have the Fed be as transparent as possible, a first step would be to provide the public with a better understanding of the Fed’s plan for averaging inflation.

Any plan they pin down won´t work!

https://marcusnunes.substack.com/p/is-the-new-monetary-policy-framework